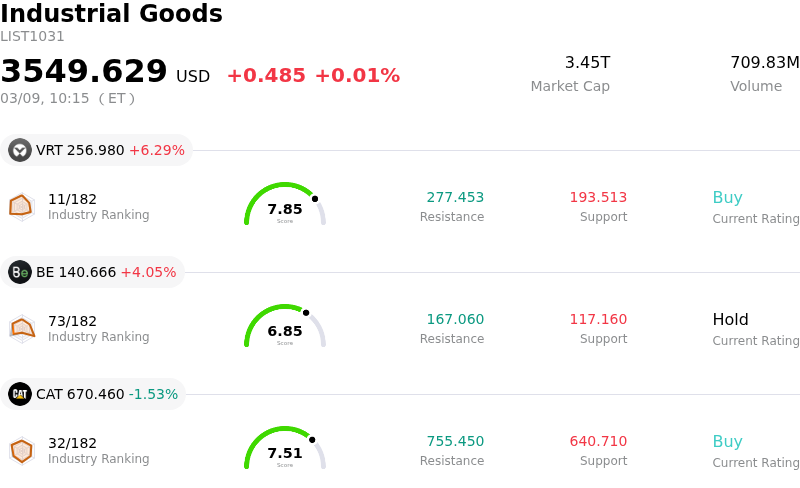

Albany International Corp (AIN) moved down by 4.41%. The Industrial Goods sector is up by 0.01%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Vertiv Holdings Co (VRT) up 6.29%; Bloom Energy Corp (BE) up 4.05%; Caterpillar Inc (CAT) down 1.53%.

What is driving Albany International Corp (AIN)’s stock price down today?

The stock of Albany International Corp. (AIN) experienced a significant downward movement, likely driven by a combination of factors including mixed earnings reception, cautious analyst sentiment, and institutional selling.

While the company reported fourth-quarter 2025 revenue that exceeded analyst expectations, the interpretation of its earnings per share (EPS) was less clear. Some reports indicated an EPS beat, while others suggested a miss of higher analyst projections. This ambiguity surrounding EPS performance could have created investor uncertainty. Adding to this, Albany International's first-quarter 2026 EPS guidance fell below consensus estimates, which likely triggered investor concern and contributed to the downward pressure on the share price.

Analyst sentiment surrounding AIN remains cautious, with a consensus rating of "Reduce" or "Hold" from various Wall Street analysts. Some analysts have even issued "Sell" ratings, reflecting concerns over future performance and a projected revenue decline for the next fiscal year. For instance, Zacks Research recently raised Albany International from a "strong sell" rating to a "hold" rating in a research note on March 3rd. However, a previous report in November saw Zacks Research downgrade Albany International from a "hold" to a "strong sell".

Furthermore, institutional portfolio adjustments have also played a role. News surfaced that Vanguard Group Inc. reduced its stake in Albany International by 1.5% during the third quarter, selling a notable number of shares. Such institutional selling can signal a shift in large investors' confidence and often leads to a negative market reaction, amplifying the downward movement. This reduction in stake by a major institutional investor like Vanguard, becoming public on the same day as the stock's decline, likely intensified the negative market reaction.

Despite these negative pressures, it is worth noting that Albany International has declared a quarterly dividend of $0.28 per share, payable in April 2026. Additionally, there have been some positive valuation adjustments, with analysts nudging their price target slightly higher, citing updated assumptions around discount rates, long-term revenue trends, and a modestly higher future price-to-earnings multiple, although the assumed net profit margin has fallen. However, the overall cautious outlook from analysts and institutional selling appear to be the primary drivers of the recent price decline.

Technical Analysis of Albany International Corp (AIN)

Technically, Albany International Corp (AIN) shows a MACD (12,26,9) value of [0.65], indicating a neutral signal. The RSI at 52.81 suggests neutral condition and the Williams %R at -26.59 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Albany International Corp (AIN)

Albany International Corp (AIN) is in the Industrial Goods industry. Its latest annual revenue is $1.18B, ranking 94 in the industry. The net profit is $-57.34M, ranking 191 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $58.00, a high of $64.00, and a low of $55.00.

More details about Albany International Corp (AIN)

Company Specific Risks:

- The company issued first-quarter 2026 earnings per share guidance below consensus estimates, signaling potential underperformance.

- Albany International faces ongoing profitability challenges, including negative trailing twelve-month earnings per share and a negative net margin, alongside signs of deteriorating financial health with negative Earnings (EBIT) and increased debt relative to equity.

- Analyst sentiment remains cautious following mixed Q4 2025 earnings, with many Wall Street analysts maintaining "Reduce" or "Hold" ratings and some issuing "Sell" recommendations, exemplified by Truist Financial maintaining a "Hold" rating.

- Operational difficulties persist due to broad demand weakness in Europe and anticipated reductions in demand for key aerospace programs like CH-53K and Gulfstream contracts, which could impede future revenue growth and margin expansion.

Find out more