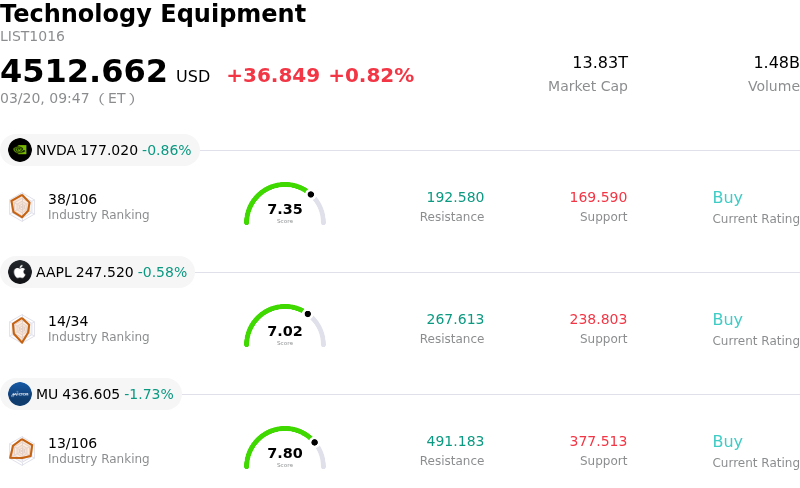

Arm Holdings PLC (ARM) opened up by 5.89%. The Technology Equipment sector is up by 0.82%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.86%; Apple Inc (AAPL) down 0.58%; Micron Technology Inc (MU) down 1.73%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

ARM Holdings experienced a notable intraday increase in its share price, primarily driven by a significant analyst rating upgrade and the company's strong positioning within the expanding artificial intelligence (AI) chip market.

HSBC upgraded ARM's rating from "Reduce" to "Buy" and substantially raised its price target to $205 from $90. This reflects a positive shift in analyst sentiment, attributing the change to ARM's strategic move towards AI-driven server processors, a transition that HSBC believes is not yet fully reflected in the company's valuation. The brokerage anticipates a "game-changing" shift from a smartphone-centric licensing model to a broader role in AI server CPUs. They project industry CPU shipments to grow significantly in 2026 and 2027, driven by rising demand for server chips tied to agentic AI.

Furthermore, the adoption of ARM's v9 architecture and Neoverse Compute Subsystems is expected to increase royalty rates per chip as major hyperscalers transition to newer designs. HSBC forecasts that ARM's server CPU royalty revenue could see a compound annual growth rate of 76% between fiscal year 2026 and 2031, potentially reaching around $4 billion by fiscal year 2031 from this segment alone. Citi analyst Andrew Gardiner also reiterated a "Buy" rating for ARM, maintaining a price target of $190, citing the rapid adoption of ARM's v9 architecture which generates significantly higher royalty rates. This new architecture is a key driver for the company's royalty revenue, which recently reached a record $737 million.

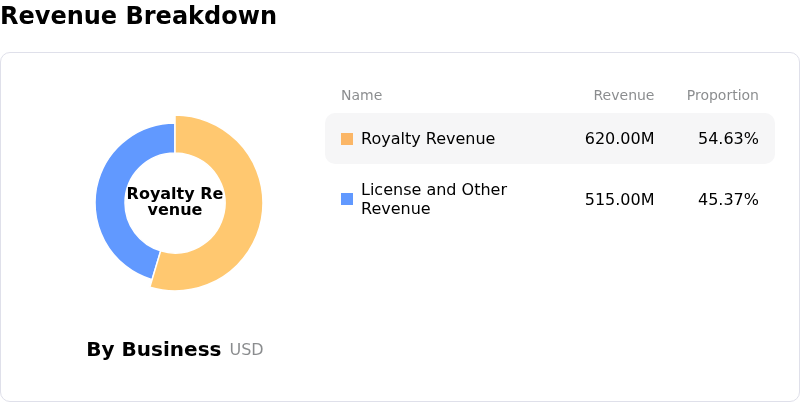

The company's strong financial performance in the third quarter of fiscal year 2026, which ended December 31, 2025, also contributes to the positive outlook. ARM reported a 26% year-over-year revenue growth to $1.24 billion, marking its fourth consecutive quarter of billion-dollar revenue. Both royalty revenue and license and other revenue saw robust growth, increasing by 27% and 25% respectively, primarily fueled by demand in AI, data centers, and advanced technologies. ARM's increasing relevance in the AI chip design ecosystem, including its role as a preferred partner for companies like NVIDIA, is also enhancing investor focus. The company is scheduled to host an "Arm Everywhere" event on March 24, 2026, which is expected to highlight its future in AI and intelligent compute, potentially further influencing market sentiment.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [0.63], indicating a buy signal. The RSI at 60.35 suggests neutral condition and the Williams %R at -5.40 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.01B, ranking 26 in the industry. The net profit is $792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $146.21, a high of $201.00, and a low of $81.78.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- ARM faces a corruption, fraud, and abuse-of-power investigation by Malaysia's anti-corruption agency over a government chip design deal signed in March 2025, posing legal and reputational risks.

- Analysts express concerns over significant overvaluation, leading to recent lowered price targets by KeyBanc and RBC Capital, as InvestingPro data suggests shares are trading above fair value.

- Projected slowing royalty revenue growth for Q4, particularly from key segments like smartphones, coupled with increasing operating expenses, is expected to pressure profit margins.

- The company's established licensing model is challenged by intensifying competitive threats from open-source architectures such as RISC-V and strategic moves by major players like Nvidia into the Windows-on-Arm ecosystem.

Find out more