Option Strategy

Option Strategy refers to a combination of positions in an account with a hedging relationship, typically a combination of options and underlying stocks. Tiger will apply some margin relief to the Option Strategy in consideration of the fact that the option strategy mitigates the relevant risks.

Option Strategy Applicable Scope

Client: The option strategy is only available to clients who meet the corresponding conditions and have opened the option strategy permissions. Please contact customer service for more details.

Symbol: US options and US stocks

Option Strategy Type and Margin

Tiger currently offers various option strategies as follows:

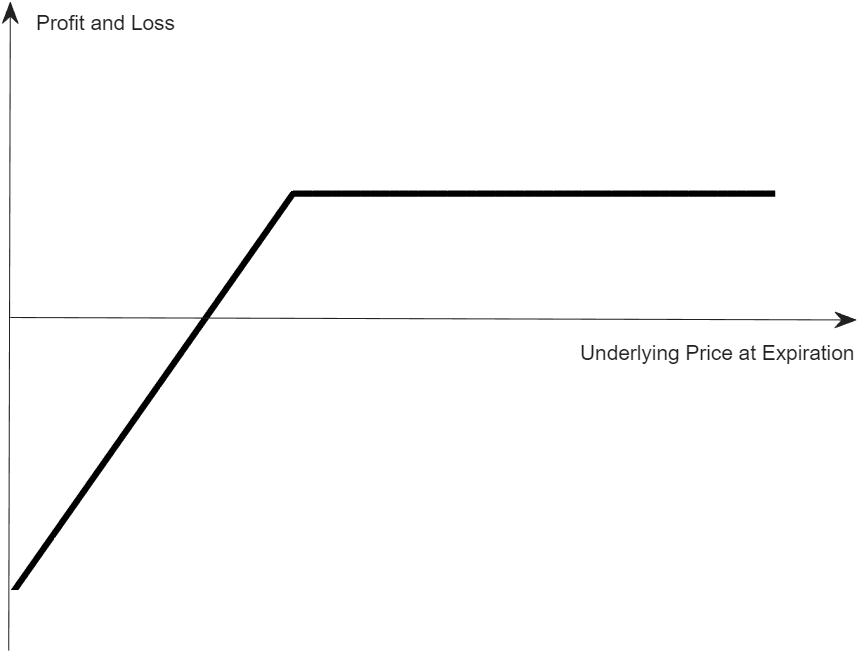

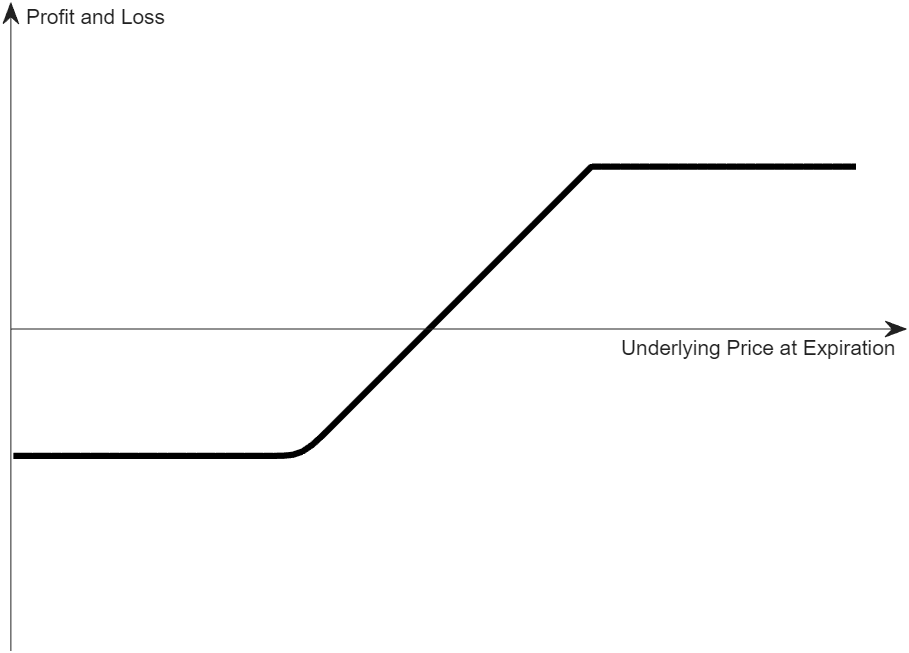

Covered Call: Short 1 call and long the underlying stock with the quantity equal to the contract size of the call.

Margin: Long Stock Margin + In-the-Money Amount of Short Call * (1 - Long stock Margin Rate)

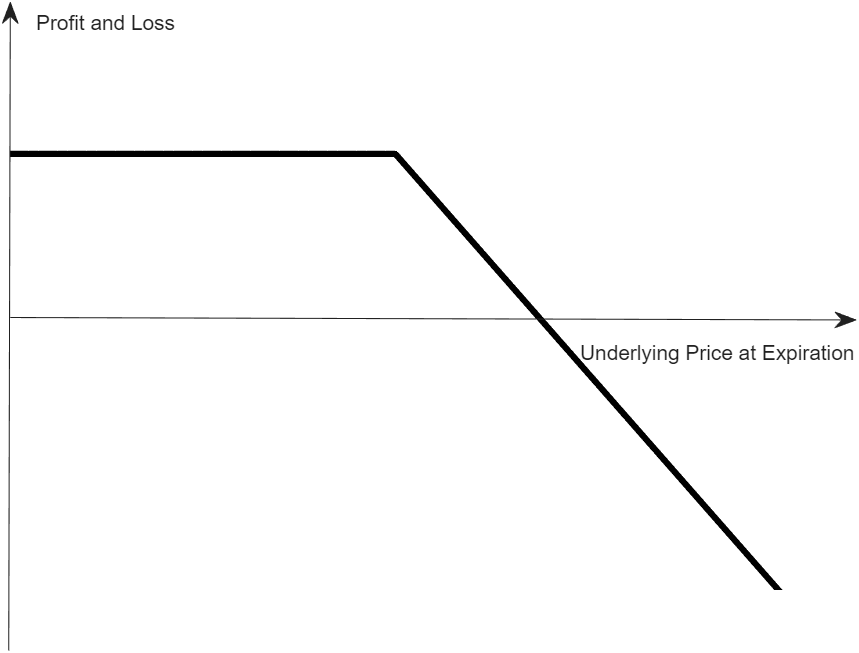

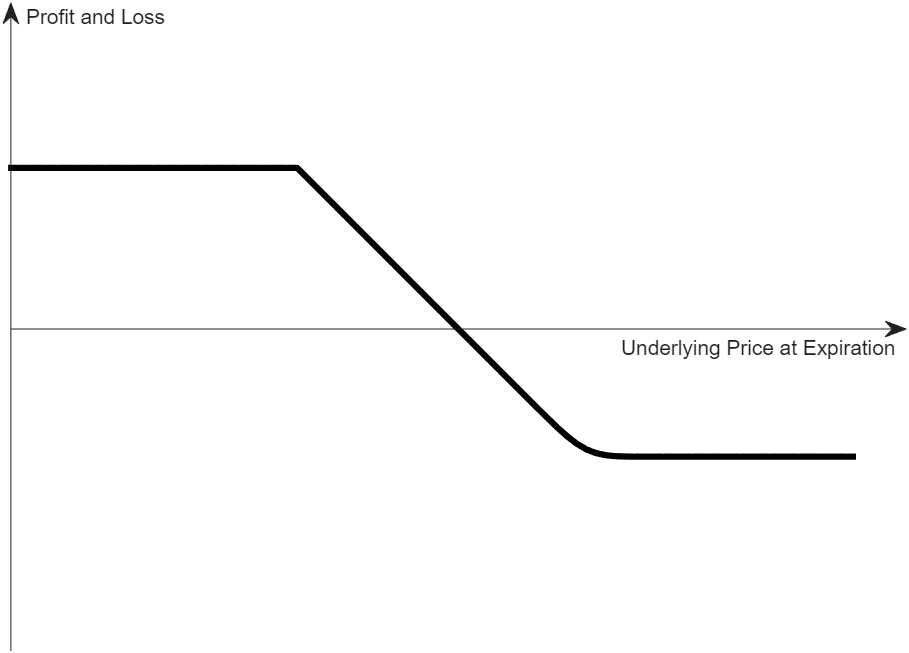

Covered Put: Short 1 put and short the underlying stock with the quantity equal to the contract size of the put.

Margin: Short Stock Margin + In-the-Money Amount of Short Put

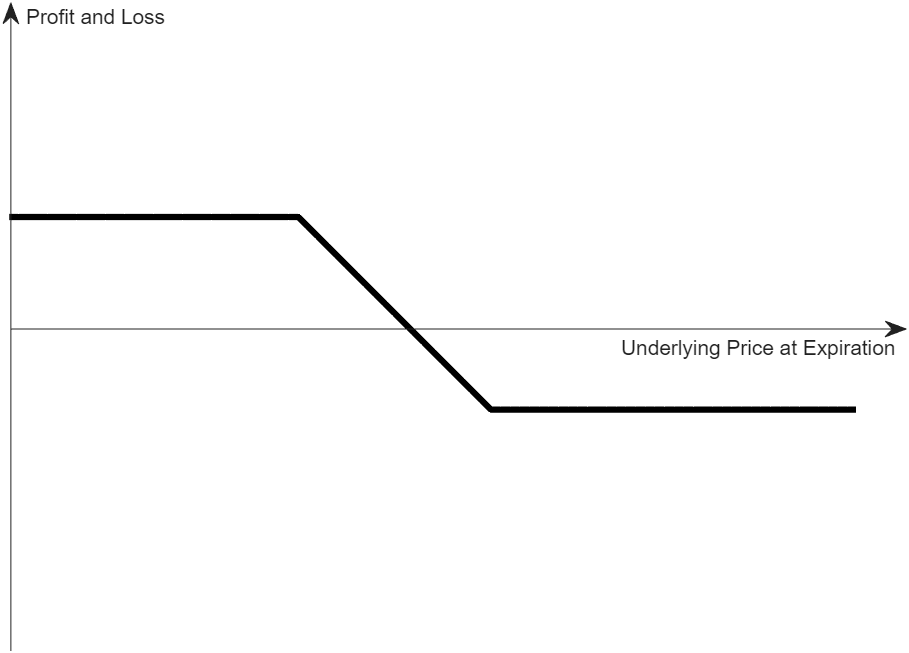

Vertical Spread:

Call Vertical Spread: Short 1 call and long 1 call, with the same underlying (stock or index) and expiration date, but different strike prices.

Margin: Max (Long Call Strike - Short Call Strike, 0) * Contract Size

Put Vertical Spread: Short 1 put and long 1 put, with the same underlying (stock or index), contract size and expiration date, but different strike prices.

Margin: Max (Short Put Strike - Long Put Strike, 0) * Contract Size

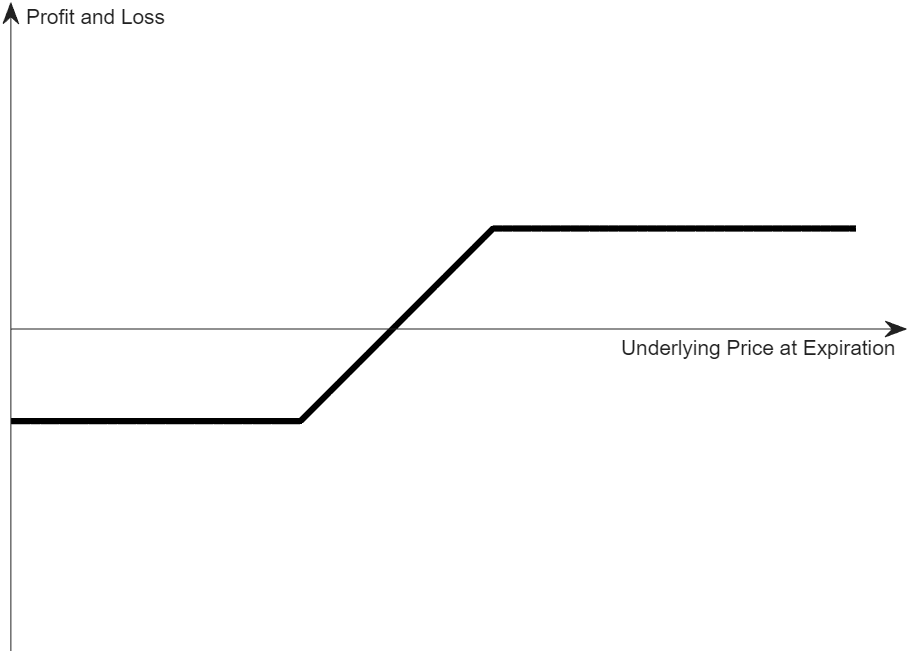

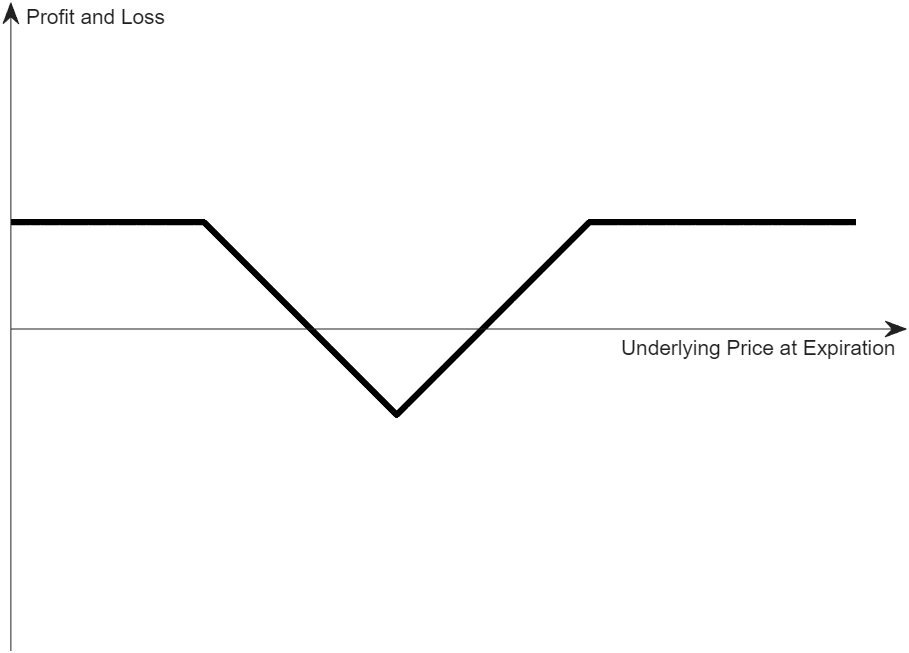

Short Strangle or Straddle: Short 1 call and short 1 put, with the same underlying and expiration date, and the put strike price is less than or equal to the call strike price.

Margin:

When the margin for the short call is greater than that for the short put: Short Call Margin + Short Put Price * Contract Size

When the margin for the short put is greater than that for the short call: Short Put Margin + Short Call Price * Contract Size

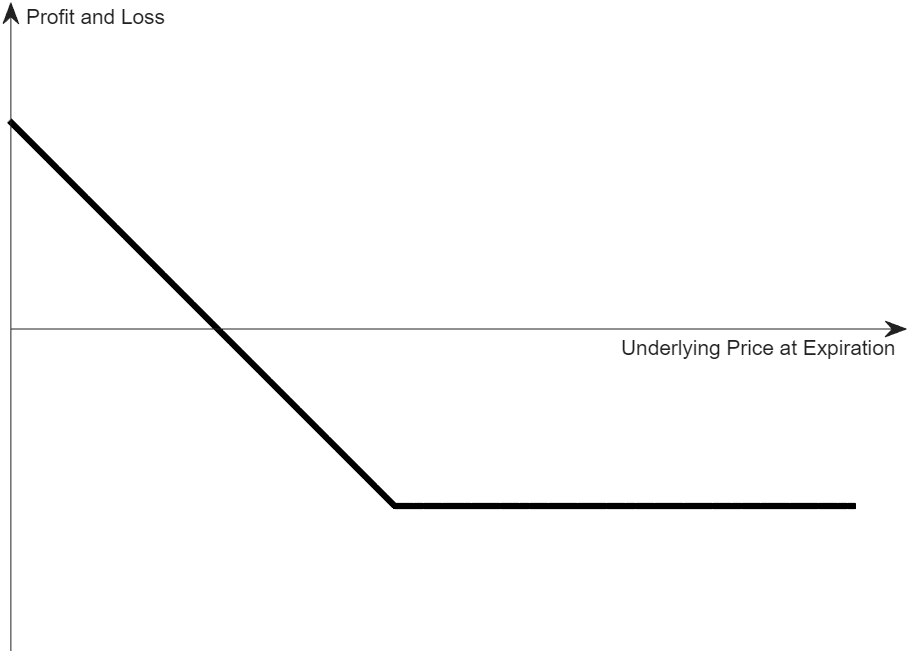

Protective Call: Long 1 call and short the underlying stock with the quantity equal to the contract size of the call.

Margin: Short Stock Margin

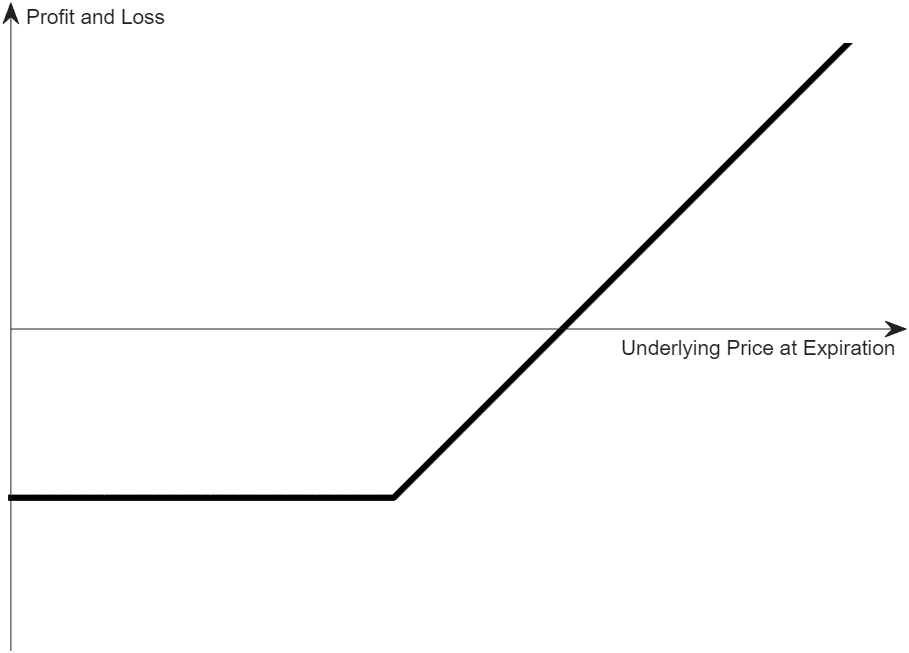

Protective Put: Long 1 put and long the underlying stock with the quantity equal to the contract size of the put.

Margin: Long Stock Margin

Calendar Spread: (No margin reduction for VIX index options)

Call Calendar Spread: Short 1 call and long 1 call, with the same underlying (stock or index) and strike price, and the short call expires earlier than the long call.

Margin: 0

Put Calendar Spread: Short 1 put and long 1 put, with the same underlying (stock or index) and strike price, and the short put expires earlier than the long put.

Margin: 0

Diagonal Spread: (No margin reduction for VIX index options)

Call Diagonal Spread: Short 1 call and long 1 call, with the same underlying (stock or index) but the strike prices may be different, and the short call expires earlier than the long call.

Margin: Max (Long Call Strike - Short Call Strike, 0) * Contract Size

Put Diagonal Spread: Short 1 put and long 1 put, with the same underlying (stock or index) but the strike prices may be different, and the short put expires earlier than the long put.

Margin: Max (Short Put Strike - Long Put Strike, 0) * Contract Size

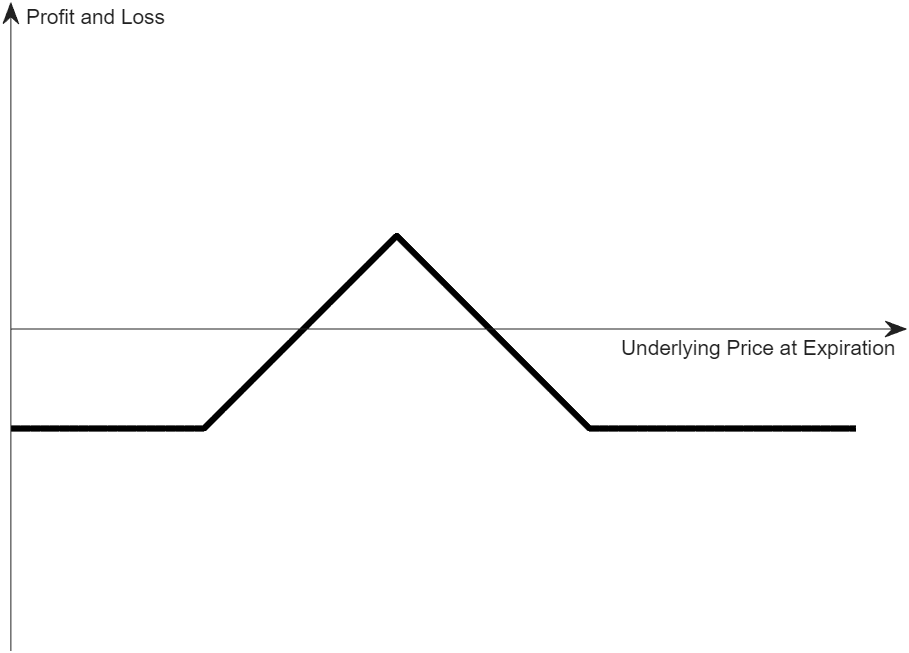

Butterfly:

Short Call Butterfly: Short 1 low-strike call, long 2 mid-strike calls and short 1 high-strike call, with the same underlying (stock or index) and the same expiration date, and the high-strike minus the mid-strike is equal to the mid-strike minus the low-strike.

Margin: (Mid-Strike - Low-Strike) * Contract Size

Short Put Butterfly: Short 1 low-strike put, long 2 mid-strike putts and short 1 high-strike put, with the same underlying (stock or index) and the same expiration date, and the high-strike minus the mid-strike is equal to the mid-strike minus the low-strike.

Margin: (Mid-Strike - Low-Strike) * Contract Size

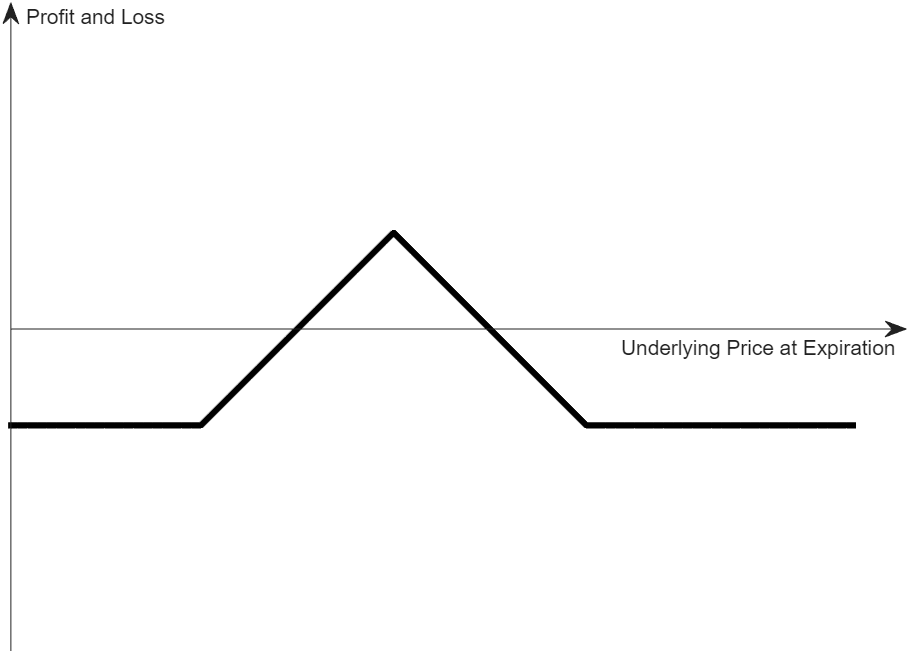

Long Butterfly: The opposite position of the short butterfly.

Margin: 0

Iron Butterfly:

Short Iron Butterfly: Long 1 low-strike put, short 1 mid-strike put, short 1 mid-strike call, and long 1 high-strike call, with the same underlying (stock or index) and the same expiration date, and the high-strike minus the mid-strike is equal to the mid-strike minus the low-strike.

Margin: (Mid-Strike - Low-Strike) * Contract Size

Long Iron Butterfly: The opposite position of the short iron butterfly.

Margin: 0

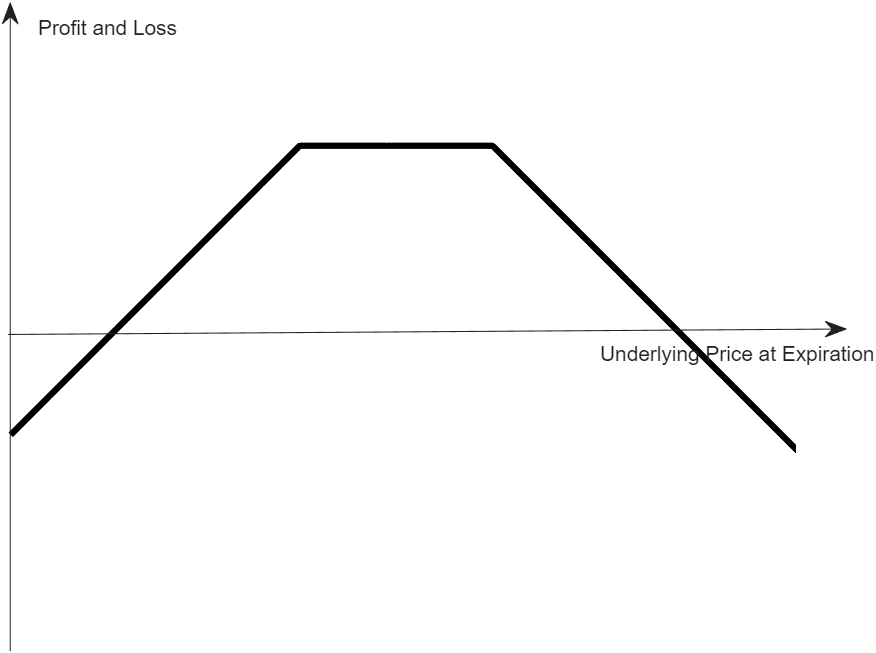

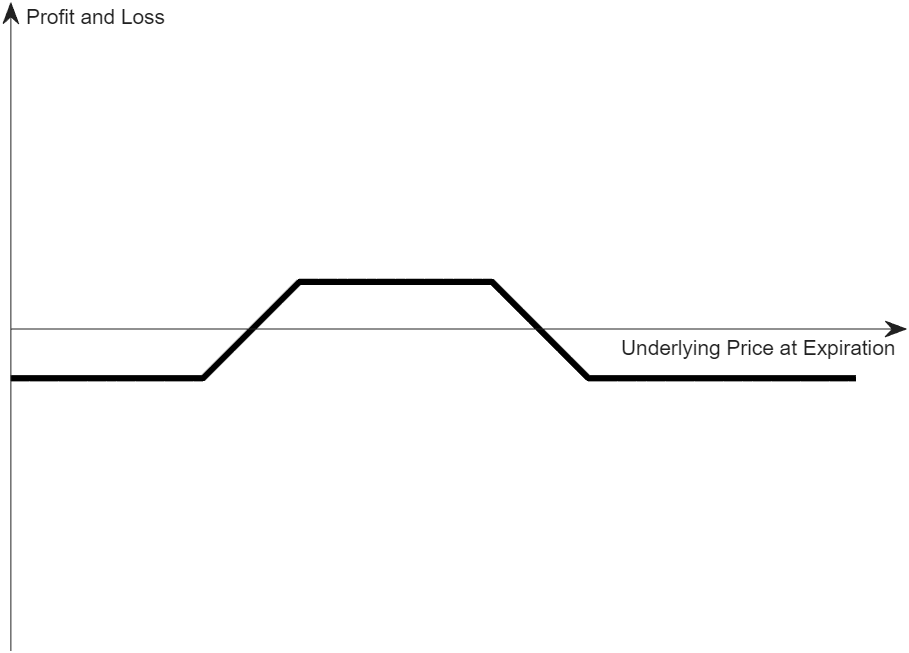

Condor:

Short Call Condor: Short 1 lowest-strike call, long 1 lower-strike call, long 1 higher-strike call and short 1 highest-strike call, with the same underlying (stock or index) and the same expiration date, and the highest-strike minus the higher-strike is equal to the lower-strike minus the lowest-strike.

Margin: (Lower-Strike - Lowest-Strike) * Contract Size

Short Put Condor: Short 1 lowest-strike put, long 1 lower-strike put, long 1 higher-strike put and short 1 highest-strike put, with the same underlying (stock or index) and the same expiration date, and the highest-strike minus the higher-strike is equal to the lower-strike minus the lowest-strike.

Margin: (Lower-Strike - Lowest-Strike) * Contract Size

Long Condor: The opposite position of the short condor.

Margin: 0

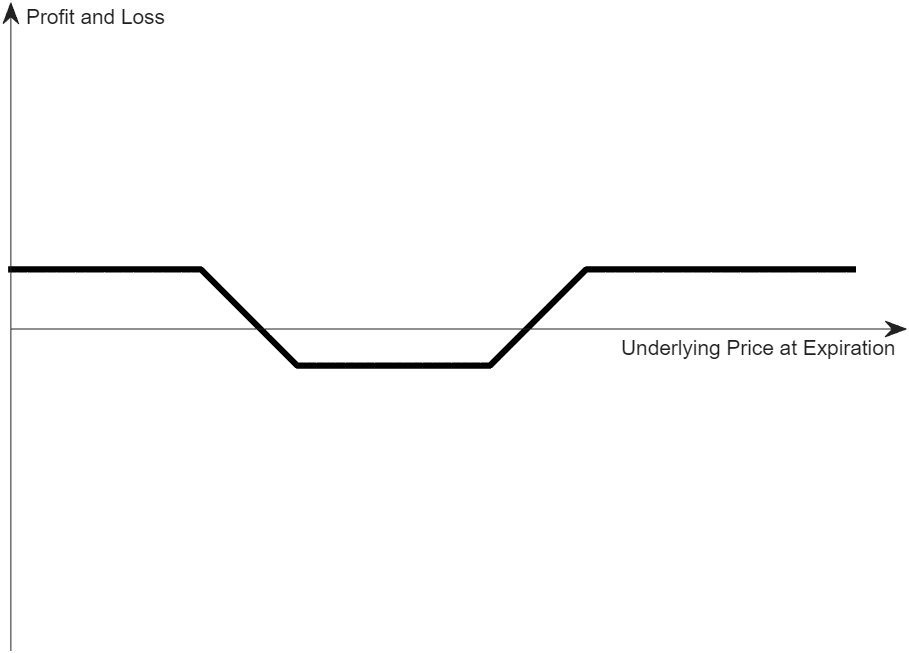

Iron Condor:

Short Iron Condor: Long 1 lowest-strike put, short 1 lower-strike put, short 1 higher-strike call and long 1 highest-strike call, with the same underlying (stock or index) and the same expiration date, and the highest-strike minus the higher-strike is equal to the lower-strike minus the lowest-strike.

Margin: (Lower-Strike - Lowest-Strike) * Contract Size

Long Iron Condor: The opposite position of the short condor.

Margin: 0

Box:

Short Box: Short 1 low-strike call, long 1 high-strike call, long 1 low-strike put and short 1 high-strike put, with the same underlying (stock or index) and the same expiration date.

Margin: Max [1.03 * Cost to Close, (High-Strike – Low-Strike) * Contract Size]

Long Box: The opposite position of the short box.

Margin: 0

Custom: You can customize the standard combinations that are not listed above, and the custom combinations can contain the above standard combinations with reasonable margin reductions. Currently, the maximum number of legs that support custom options is 4.

Details about Option Strategy Margin:

If your newly held options or stocks can constitute an option strategy with your existing positions, the margin requirements for the positions in your option strategy may be reduced. Tiger will make adjustment to the margin requirements based on market risk levels, liquidity, options expiry dates, position conditions and other factors, and reserves the right to liquidate any leg of the portfolio without prior notice.

Margin requirements will not be less than the cost to close all legs of the portfolio.

If you liquidate part of your position in the option strategy, the option strategy will be invalidated and you will no longer be offered margin relief, which may result in deterioration of the risk-control value in your account. Please ensure that you have sufficient funds in your account before liquidating your position in the option strategy as forced liquidation may occur when EL<0.

If you need to liquidate part of your positions in the option strategy, we recommend that you liquidate the option positions in the option strategy first in order to avoid an increase in margin caused by the liquidation action; if you liquidate the stock positions in the option strategy first but only partially filled, it will cause the option strategy to lapse and there will be both option positions and stock positions in your account, thus the sum of the margin of both positions will be higher than the margin requirement of the option strategy, which will increase the margin of your account.

If you hold an option strategy that is approaching expiration, due to the risk of exercise of short options, the probability and amount of additional margin requirements for your options portfolio position will increase as the expiration date approaches, the proportion of the short options' market value in total assets increases, and the degree of being in-the-money increases. It is recommended that you pay attention to the risk associated with approaching expiration.

Please note that the option strategies cannot currently be applied to some positions whose relevant symbols or contract multipliers have changed due to corporate actions such as split and merger. If a position in the option strategy is subject to such corporate action, this may result in the option strategy invalidating and thus increasing the margin requirement. Please ensure that you have sufficient funds in your account before liquidating your position in the option strategy as forced liquidation may occur when EL<0.

If you hold the vertical spread, diagonal spread, (iron) butterfly, (iron) condor, box or other option strategies through expiration: if the underlying price closes between the strikes of different legs at expiration, your short leg may be assigned and your long leg may expire worthless. Be cautious of this scenario: if your short leg is assigned, you'll be left with unhedged stock positions with undefined risk. Meanwhile, your long option will no longer exist to hedge the risk. This may potentially result in losses greater than the theoretical max loss of the option strategy.

Important: To help mitigate this risk, Tiger may close your position prior to market closure on the expiration date; however, this is done on a best-effort basis. Ultimately, you are fully responsible for managing the risk within your account.